Financial goals 2024 — 11 investing and personal finance goals focussed on frugality and efficiency for 2024. I am not a licensed investment advisor and this post is not investment advice. All opinions are my own.

Welcome to my financial goals for 2024.

For the record, I have been publishing my annual financial goals on this blog since 2017.

This year, however, I have been debating if it even makes sense to continue sharing my financial goals publicly.

But I ultimately decided to continue the tradition because it’s something I enjoy and it works.

“Figure out what works, and do it.” — Charlie Munger

As always, I aim to focus on specific, measurable, achievable goals.

Of course, each year has its own set of circumstances.

Last year, after purchasing my first home, my focus was on financial organization because there were many unknown variables.

In 2024, I’m ready for a year of efficiency and frugality. I want to build on the financial organization I set up in 2023 and refine my spreadsheets. I want to ruthlessly cut back spending on the areas that don’t bring value. And of course, I want to continue growing my dividend income and building my investment portfolio.

In this post, I will share the specific financial goals I am focusing on in 2024.

First, I want to elaborate on the theme for my 2024 financial goals.

Financial Goals 2024 Theme

If I had to sum up the theme for this year’s financial goals in two words, it would be efficiency and frugality.

Ultimately, I am building on the foundation that was set in 2023.

In case you missed my financial goals for 2023, you can read the full blog post here.

As mentioned earlier, the theme for 2023 was financial organization.

I am very satisfied with how that focus turned out.

I literally tracked every single dollar I spent — I could tell you the exact amount I spent on the smallest expense. This attention to detail set up 2024 perfectly for a year of frugality and efficiency. It’s quite eye opening to see how much small amounts add up over a year.

Other than building on last year’s financial organization, there are macro factors that are contributing to my focus. For example, some economists are predicting a recession in 2024. At the very least, most are expecting a slow down. Hence why the U.S. Federal Reserve kept its key rate unchanged in December and signalled rate cuts could be coming.

Of course, macro events will not change my long-term investing strategy. But it doesn’t hurt to be cautious and have additional cash for emergencies and also as portfolio insurance to avoid selling stocks at an inopportune time.

Otherwise, the Canadian housing market is a small consideration in this year’s theme. Fortunately, my mortgage is on a fixed rate until 2027. The rate is also considerably lower than my investment returns and current interest rates, so paying it off early rather than investing is not even a consideration. But one small risk I am susceptible to is that I live far from my job. I am lucky that I get to work from home most of the time. However, there is always a small risk that things could change. As such, I have been keeping a close eye on the real estate market and developing an exit plan just in case. Simply put, I want to have plenty of cash available just to be extra prepared.

One other small consideration is that my household is DITC (double income two cats). I have two new dependents (cats) to care for now, so it’s important to have a proper emergency fund.

Financial Goals 2024

My annual financial goals are always built around my long-term ambition to become financially independent.

To be clear, I am not aiming for financial independence retire early (FIRE). I simply want to gain independence and autonomy.

The reason I mention this is to provide context for how I decided on the framework.

After assessing each year’s progress, discussing personal finance with my partner in our annual financial meeting, and factoring in my long-term goals, I decide on how to approach financial goals.

I typically begin with investment goals before moving on to personal finance goals. My 2024 financial goals follow that same pattern, except for one personal finance goal that was squeezed in between my investment goals to accommodate this year’s theme.

Without further ado, let’s get to my financial goals for 2024.

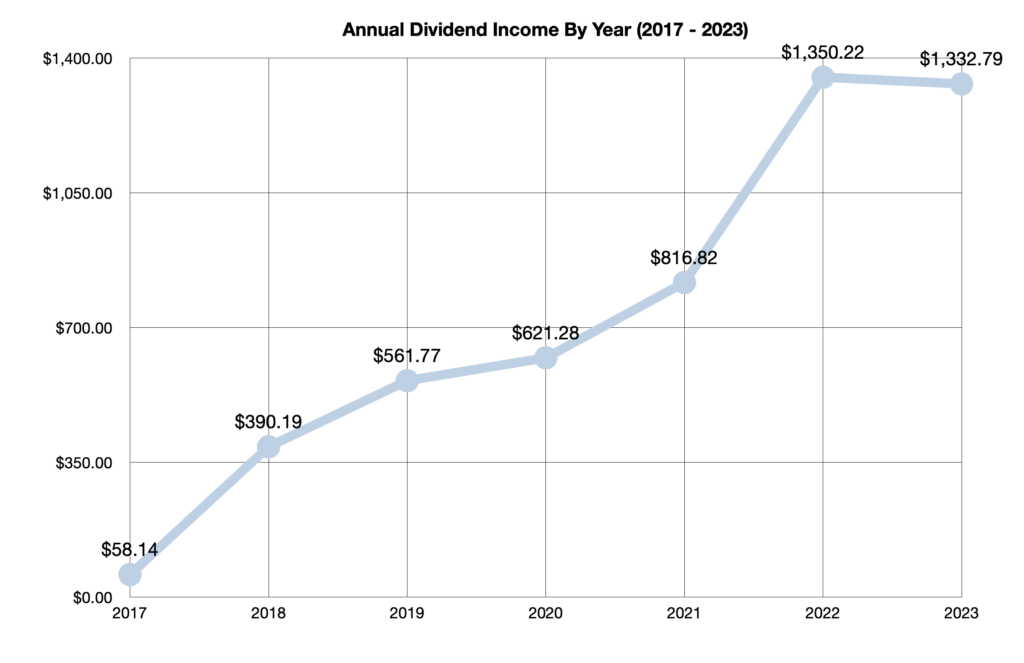

1. Earn $2,000 In Dividend Income (34% Year-Over-Year Growth)

Since dividend investing is such a central part of my investment strategy and long-term goal to become financially independent, I always start with my dividend income target when setting annual goals.

My goal in 2024 is to earn at least $2,000 in dividend income.

After setting a more modest target in 2023, following the purchase of my first home, I am ready to aim higher again.

This $2,000 dividend income target represents a 34% year-over-year increase compared to how much dividend income was earned in 2023. It’s a sizeable increase compared to the 3.7% target I set in 2023.

To reach this goal, I will need to average around $167 per month in dividends. Of course, I will continue to blog monthly dividend income updates to document the progress.

To achieve my $2,000 target, I will rely on the three dividend growth levers (reinvesting dividends | dividend raises | investing new capital). This year, however, reinvesting dividends and dividend raises are expected to do more of the heavy lifting.

Frankly, I could be setting a much higher target based on my current PADI (projected annual dividend income). However, I do not plan on utilizing all three dividend growth levers to their full extent. I will continue to reinvest all dividends, and dividend raises will increase PADI automatically. But the new capital lever will not be fully used for dividend investing. As I alluded to earlier, I want to have plenty of cash available as portfolio insurance. So more of this year’s savings will be put in cash accounts or cash-like investments such as money market funds. Surely, I will continue to save and invest new capital in dividend stocks. It’s just that I will save more cash than usual.

This leads into the next goal.

2. Build Up Emergency Fund & Accessible Cash-Like Reserves

Candidly, my emergency fund is already the largest it has ever been because I don’t want to ever have to interrupt the compounding process again.

“The first rule of compounding: Never interrupt it unnecessarily.” – Charlie Munger

Prior to owning a home, I invested most of my savings in stocks and kept a very small emergency fund, if any at all. But life has changed a lot over the past few years. I have a property, a vehicle, and two cute cats.

In turn, having an emergency fund has become more of a priority.

Of course, the downside of holding more cash instead of investing is that it slows down growth.

But if it prevents me from ever having to sell stocks at an inopportune time, it could actually increase my returns over the long term.

Ideally, I am working towards a 6-month personal emergency fund, a joint emergency fund (covers car repairs, house maintenance, and cats), and enough accessible cash to fund a deposit on a new house (just in case). This is aside from my sinking fund (covers spending, gifts, vacation).

Perhaps this is too meticulous and too much cash that will not be invested in equities earning higher returns. But by next year when I’m closer to my ideal cash position, I can become more aggressive with investing. The other fortunate thing about my position is that I’ve already built a portfolio that saves for me. So even if I focus on saving cash for a year, I still get to keep investing in stocks through reinvesting dividends.

3. Grow PADI (Projected Annual Dividend Income) To $2,200

I added close to $750 in PADI during the course of 2023.

At that pace, I should be aiming to add $800 to $1000 in annual dividend income in 2024. This would get my PADI to around $3,000.

Instead, I decided to set a modest target of $2200 in PADI by the end of 2024.

As you can probably guess, the main reason is that I want to build up my emergency fund and cash-like reserves.

But that doesn’t mean I will stop investing entirely — I have to invest. Some people look forward to going to restaurants and buying designer clothes. I look forward to buying stocks and updating my spreadsheets.

As such, I am still aiming to allocate new capital for investing in 2024. The number I have in mind is about one third as much as I invested in 2023.

Overall, the combination of dividend raises, reinvesting dividends, and investing new capital will help grow my annual dividend income to at least $2200 in 2024.

4. Spend 0.08% Or Less On Commissions In Retirement Portfolio

I try to keep my investment expenses as low as possible because fees can eat into returns over a long time frame.

As such, I am setting a goal to spend 0.08% or less of my portfolio’s value on commission fees in my retirement accounts.

To determine this target, I looked at my portfolio’s expenses in 2023 and compared to a low-cost S&P 500 ETF, VFV, as a benchmark. Since the management fee on VFV is 0.09%, my target is to spend 0.08% of my portfolio’s value on commissions and investment expenses.

Of course, my 0.08% target will not include management fees of the ETFs I am invested in. I am specifically referring to commission fees. I hold a few ETFs that have management fees, but most of them are low. For example, the management fee on VFV is only 9 basis points, and XEI is 22 basis points. Admittedly, I own a few ETFs that are higher, such as FIE, ZDI, JEPQ, and ZWC. Then again, those ETFs pay out very high yields.

Nonetheless, my goal for my retirement accounts is to spend 0.08% or less on commission fees. To accomplish this, I utilize Wealthsimple for Canadian stocks to pay zero commissions and pay for U.S. trades with credit card points.

5. Save A Minimum Of 17% Of Net Income

Since I work a job with fluctuating hours, I usually aim for a lower savings rate goal rather than set myself up for failure.

For example, I set my savings goal at 15% in 2022 but ended up saving over 25%.

In 2023, I set the goal 1% higher at 16%. I wanted to improve over the previous year while simultaneously remaining cautious due to all unknown variables after purchasing a house. Fortunately, I was able to overachieve that target again by a considerable amount. I ended up saving close to 30% in 2023, including my sinking fund. It would be even higher if I included dividend income.

But even though I have overachieved by double digits over the past two years, I am still going to remain cautious.

As such, I am setting my minimum savings goal at 17% of my net income in 2023. This is still one percent higher than last year’s goal. Hopefully I overachieve again.

6. Lower Restaurant Spending ($775 Maximum)

One of my cost-saving goals in 2024 is to keep all restaurant spending to $775 or less. Frankly, I still think this amount is too much.

But I am trying to be realistic and lower restaurant spending in a way that does not negatively affect relationships.

Personally, I would be fine with spending zero on restaurants because I don’t get a lot of value from them. Most of the time, I end up disappointed. Either the food quality is low, the restaurant is unclean, or the service is bad. You’re basically paying $100 for an Instagram photo at this point. Consequently, I prefer homemade meals from Costco while watching Financial Audit by Caleb Hammer.

Of course, I can’t just say no to every birthday meal and I have to leave some room for dates with my partner/gf/wifey. Hence why I am still prepared to spend up to $775 on restaurants this year.

For comparison, I spent $1218.33 on restaurants in 2023. Compared to 2023, my 2024 goal would equal a reduction of $443.33.

The method used to decide on $775 was quite simple. I added up all the potential birthday meals and dinner dates. Then I added in a few more dollars for unexpected restaurant spending.

For the record, the restaurant category includes going to restaurants and takeout. It does not include coffee shops.

7. Lower Coffee Shop Spending ($50 Maximum)

Another area I plan to cut back spending in 2024 is on coffee shops. Despite being a proud Starbuck’s shareholder, my goal is to keep coffee shop spending to less than $50 during the year.

Again, I think this number is still too high. I mean, I’ve only spent $5.06 on coffee shops over the last four months of 2023. But again, I want to leave some room for dates and coffee outings.

To be clear, I am not planning to cut back my coffee spending at home. I am a total coffee addict. I typically drink 3 to 4 cups per day at home. My preference is drip roast with oat milk to ensure the coffee is fresh and cost effective. But we also have a Nespresso at home for fancier coffee. It’s basically for special occasions. In truth, I enjoy drip roast more.

For comparison, I spent $137.46 on coffee shops in 2023. My $50 maximum goal will save $87.46 in 2024.

To accomplish this goal, I will only buy coffee out if it’s a date or outing. Otherwise, I’m perfectly fine making coffee at home. On days that I have to go to the office, I absolutely refuse to pay for coffee. It’s rushed and not even enjoyable. To avoid buying coffee out, I take a travel mug and buy just-in-case energy drinks from Costco in bulk. It saves time and money.

8. Decrease B.S. Spending

Another key area I want to cut back spending is going to be defined as B.S. spending. I’m sure you can guess what the acronym stands for.

Simply put, B.S. spending includes everything that I don’t actually need.

Snacks

For example, I spent $80.27 in 2023 on snacks (chips/chocolate). Over the course of the year, it’s only $6.69 per month. It’s really not that unreasonable. But that $80.27 is gone and all it did was make me unhealthier. My goal is to keep snacks under $35 in 2024.

Clothing/Shoes

Otherwise, I consider clothing/shoes to be B.S. spending, unless I actually need them. Obviously, looking nice is important. It can affect social status, confidence, and even an individual’s professional career. But it’s important to be aware of the psychology behind it all. To put it bluntly, it can be challenging to not care what people think. Hence why it really comes down to prioritizing values. If you value clothes and designer brands, by all means, feel free to spend money on it. In my case, though, I’m perfectly fine with someone thinking I look like a loser because I’m wearing a $12 Costco sweater. I’d rather have independence and autonomy than validation. To save money on clothes and shoes, I’m a minimalist who mostly shops at Costco or Uniqloo. In total, I spent $287.84 on clothing/shoes/coats in 2023. My goal for 2024 is to spend less than $250.

Alcohol/Debauchery/Shennanigans

Other than that, B.S. spending includes things like alcohol and recreational cannabis, which I don’t spend much on nowadays. I mean, my annual alcohol spending is probably less than some people spend in a weekend. I drank a lot in college because I’m an introvert and it helped socially. But I really don’t have much of an interest in it now. Are you ready for my total alcohol spending in 2023? I spent a shockingly low $63.08 on alcohol. My goal in 2024 is to spend $50 or less.

Lastly, one other category I am planning to cut back on in 2024 is recreational cannabis. As a Canadian, recreational cannabis is legal. And if I’m being honest, it’s one of my favourite indulgences. But I also realize it is not a sustainable hobby to continue in older age. I mean, I can’t smoke weed all the time in my fifties and sixties. As such, I’ve been tapering off my consumption over the last few years. But I still spend way too much on it. In total, I spent an embarrassingly high $961.55 on cannabis this past year. Ideally, I want to reduce that to $500 or less. Frankly, that’s still embarrassingly high.

9. Keep Bank Fees To $93.40 Maximum

As I mentioned earlier, it’s truly eye opening to see how much you spend when you track every single dollar.

For example, I spent $258.41 on bank fees in 2023.

As someone who worked in the banking industry at two Canadian banks for over seven years, this is ridiculous and embarrassing.

I spent $16.95 a month on my chequing account and was paying an overdraft protection fee, which is a service I don’t even use! I use credit cards for almost every transaction and pay them off every payday.

As such, I cancelled my overdraft protection and plan to limit my transactions to cut fees back to $6.95 per month. This should limit my spending to $93.40 maximum in 2024.

10. Prioritize Near-Term Category Saving In Sinking Fund

In addition to retirement and emergency savings, I started a sinking fund in 2023 to save for gifts, vacations, life events, and for random spending.

For the most part, having a sinking fund has worked out well. However, there are a few changes I plan to implement in 2024.

The main change is that I will prioritize near-term category saving instead of trying to save for everything at once.

During the course of 2023, I contributed 1 to 2% to each category per pay. Although this worked better than not having a sinking fund, I found that it left me short in some categories. For example, I didn’t have enough for Christmas so I had to allocate more in November.

As such, the solution I have come up with is to prioritize near-term spending categories instead of trying to save for everything at once.

For example, I stopped saving for vacations over the last few months in order to save more for Christmas spending.

In the new year, I plan to save for the category that will require spending next. Once I have saved enough for that category, I will move on to the next category.

11. Read 5 Books —The Most Important Thing | Same As Ever | The Single Best Investment | The Options Wheel Strategy | Atomic Habits

I usually read a few books per year and reread my favourite books. But I rarely set reading goals because I listen to a lot of podcasts and Youtube for my financial content.

However, I decided to challenge myself this year and add a few more books to my collection.

My goal is to read the following 5 books:

- The Most Important Thing by Howard Marks

- Same As Ever by Morgan Housel

- The Single Best Investment by Lowell Miller

- The Options Wheel Strategy by Freeman Publications

- Atomic Habits by James Clear

Ultimately, I feel like these books will provide a good mix of learning about new topics and building on my investment knowledge.

I have been interested in reading The Most Important Thing by Howard Marks since I discovered how quotable the book is.

Same As Ever by Morgan Housel is a must read because The Psychology of Money is the best personal finance book ever written. Morgan Housel is a fantastic writer and has an incredible ability to simplify complex topics.

The Single Best Investment by Lowell Miller is a book on dividend growth investing. I’ve already started reading the pdf online and have been thoroughly enjoying it.

The Options Wheel Strategy is a book to satisfy my curiosity and learn more about options. The Wheel Strategy is an options strategy that is appealing, because I am comfortable with stock price fluctuations and holding stocks for long periods of time. In my case, I could utilize the wheel strategy to sell cash-covered puts on stocks I am already interested in. If the option contract expires without being exercised, I could collect options premiums. If the option contract gets exercised, I would be obligated to own the stock at a price I would be happy to buy it at. Then I could just sell a covered call on the same stock to collect options premiums until I am obligated to sell it. Anyways, I’m not sure at this point if options trading is something I’m willing to do. But I’m interested enough in this strategy to read more about.

Finally, I plan to read Atomic Habits by James Clear, which is a personal development book. It has been highly recommended and is suitable to my personality. My financial goals, dividend income investing, workout routine, and just the way I approach anything is all centred around small steps and incremental progress.

Final Thoughts — Financial Goals 2024

In summary, the theme for my 2024 financial goals is efficiency and frugality.

I tracked every single dollar I spent in 2023. Now I want to cut back on the spending that doesn’t bring value.

In turn, I set the following 11 financial goals for 2024:

- Earn $2,000 In Dividend Income (33% Year-Over-Year Increase)

- Build Emergency Fund & Accessible Cash-like Reserves

- Grow PADI (Projected Annual Dividend Income) To $2200

- Spend 0.08% Or Less On Commissions In Retirement Accounts

- Save A Minimum Of 17% Of Net Income

- Lower Restaurant Spending ($775 Maximum)

- Lower Coffee Shop Spending ($50 Maximum)

- Decrease B.S. Spending

- Lower Bank Fees ($93.40 maximum)

- Prioritize Near Term Category Spending In Sinking Fund

- Read 5 Books

If I stick to these goals in 2024, my dividend income portfolio will generate at least $2000, my emergency fund and financial foundation will be stronger than ever, and I’ll cut back over $1000 worth of wasteful spending.

Ideally, these financial goals for 2024 will help me move closer towards achieving my long-term ambition of becoming financially independent.

Thank you for reading and best of luck with your financial goals in the New Year!

Stay tuned for more monthly dividend income updates in 2024.

Previous Financial Goal-Setting Posts

I am not a licensed investment or tax adviser. All opinions are my own. This post may contain advertisements by Monumetric and Google Adsense. This post may also contain internal links, affiliate links to BizBudding, Amazon, Bluehost, and Questrade, links to trusted external sites, and links to RTC social media accounts.

Connect With Dividend Income Investor

Instagram: @dividendincomeinvestor_

Threads: @dividendincomeinvestor_

Pinterest: @dividendincomeinvestor

Facebook: @Reversethecrushblog

Dividend Income November 2023 — $121.94 (18% YoY Growth)

Dividend Income November 2023 — $121.94 (18% YoY Growth)